Stablecoin Regulation Impact 2025: Market Shifts & Competitive Dynamics

On July 18, 2025, U.S. President Trump officially signed the GENIUS Act into law, ushering stablecoins into a new developmental phase. Currently, the global stablecoin market is undergoing profound transformation and intense competition, with its future trajectory being shaped by progressively refined regulatory frameworks (including new regulations like the U.S. GENIUS Act) and continuously enhanced compliance standards.

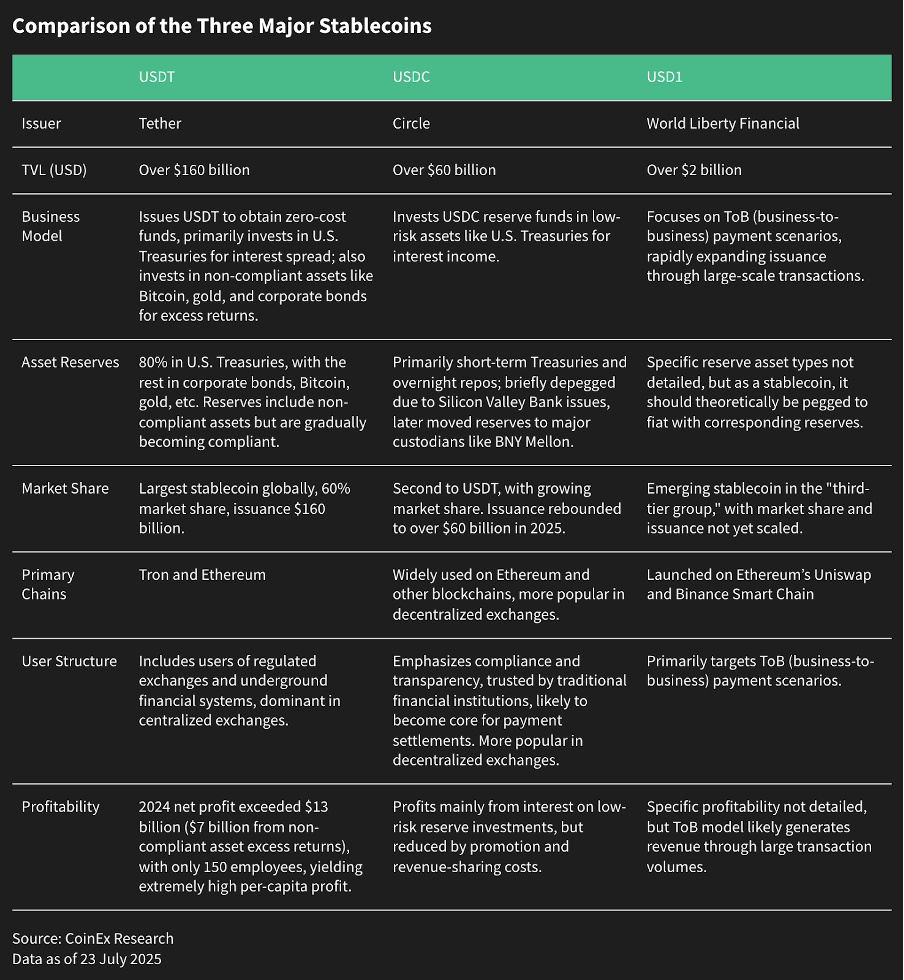

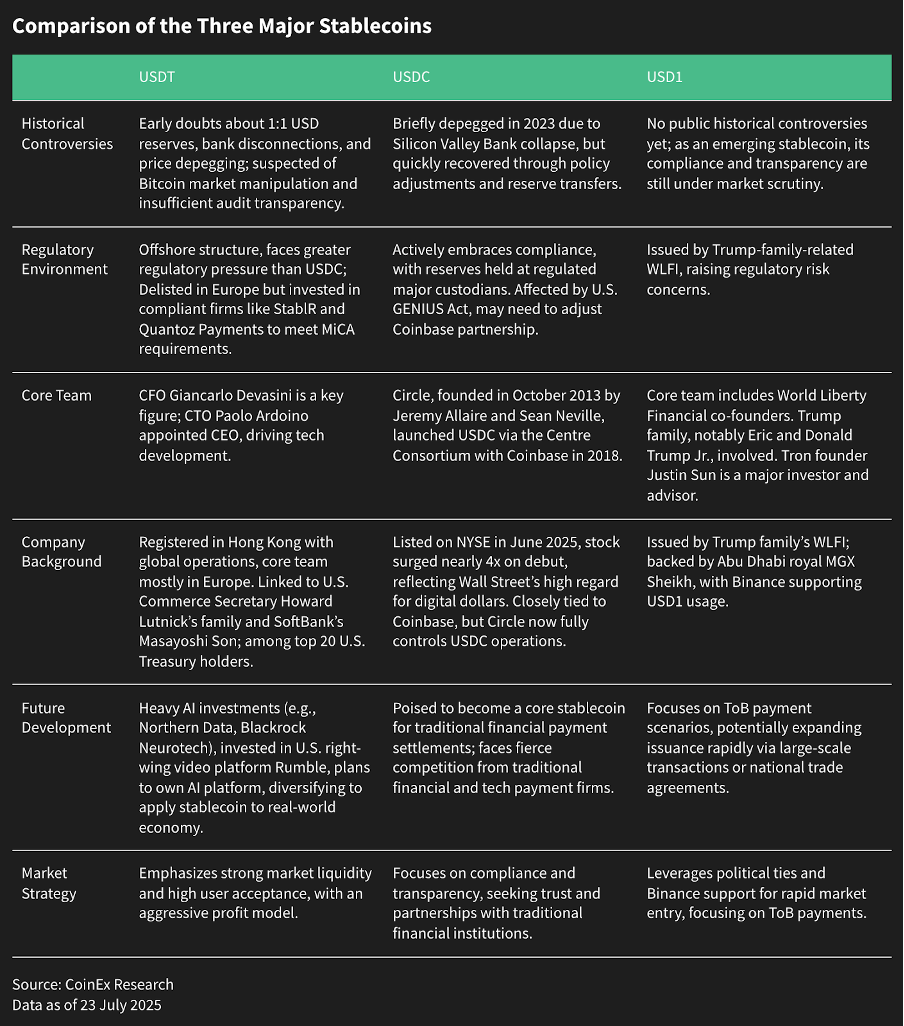

In this context, the cryptocurrency market has gradually formed three major camps represented by Tether’s USDT, Coinbase-Circle’s USDC, and USD1 launched by the Trump family. USDT has achieved substantial profits through its unique investment strategies and efficient operations; USDC has gained the trust of traditional financial institutions with its exceptional compliance and transparency, successfully going public; while USD1, leveraging its special background, has rapidly expanded into the B2B payment market. Each of the three adopts differentiated strategies, engaging in fierce competition to dominate the market.

Meanwhile, stablecoins are emerging as a crucial bridge between traditional finance and the blockchain world, becoming the central focus for global enterprises in driving fintech innovation and payment transformation. In 2025, numerous traditional companies have accelerated their strategic deployments in the stablecoin payment sector, including fintech giants, retail and technology leaders, banks, financial institutions, and technology infrastructure providers. This has led to the continuous expansion of stablecoin application scenarios and steady progress in compliance.

In this report, CoinEx Research will systematically outline the regulatory frameworks for stablecoins in three major global regions, provides an in-depth analysis of the stablecoin market landscape and the business models and market sizes of the three leading stablecoins, and focuses on the strategic deployments of traditional enterprises in the stablecoin payment sector. Additionally, through a detailed examination of the solutions, technical architectures, application scenarios, and compliance progress of several representative traditional companies, the report further explores the future opportunities in the stablecoin space and its driving force on related industry chains. It reveals the profound impact of stablecoins’ transformation from crypto-native assets to global payment infrastructure, empowering financial innovation.

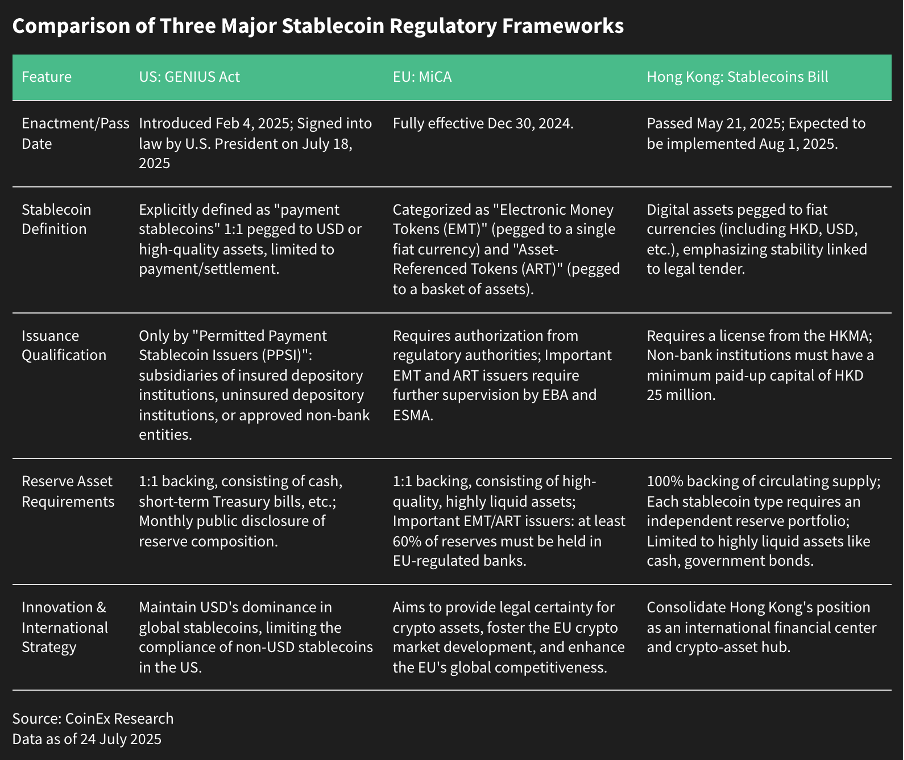

1. Global Stablecoin Regulatory Frameworks Compared: U.S. GENIUS Act, EU MiCA, and Hong Kong Stablecoin Bill

The following table visualizes the regulatory core differences and macro policy implications.

1. U.S. GENIUS Act: Dual Assurance of Dollar Hegemony and Financial Stability

Advantages

The Act aims to end the current fragmented state-level regulation in the U.S. by providing a unified federal framework for stablecoins, which will greatly enhance market certainty and attract more compliant enterprises to develop domestically. By clearly defining stablecoins as payment instruments rather than securities, it avoids potential conflicts with the SEC, removing obstacles for industry growth. Strict 1:1 reserve requirements, transparency disclosures, and bankruptcy priority rules will significantly boost investor confidence.

Highlights: Impact on U.S. Treasury Bonds

The Act requires stablecoin issuers to back their reserves with high-quality liquid assets such as U.S. Treasury bonds. This means the growth of the stablecoin market will directly increase demand for U.S. Treasuries. Treasury Secretary Janet Yellen even estimates that stablecoins could attract up to $2 trillion in new demand, helping to finance deficit spending. This undoubtedly provides a new support channel for the U.S. government’s fiscal strategy and further consolidates the dollar’s status as the global reserve currency.

Challenges and Impacts

The Act excludes stablecoins that generate yields or interest, aiming to reduce speculative risks and avoid classification as securities. However, this may limit the application potential of stablecoins in innovative scenarios like DeFi and conflicts with existing models like USDT, which generate profits through yield. Meanwhile, strict compliance requirements for foreign stablecoins (e.g., USDT) mean that issuers wishing to operate in the U.S. market will face significant adjustment pressures. After the Act’s passage, it is expected to have a profound impact on the global stablecoin market landscape, further reinforcing the dollar’s central role in the digital asset space.

2. EU MiCA: A Pioneer Prioritizing Compliance and Financial Stability

Advantages

As the world’s first comprehensive regulatory framework for crypto-assets, MiCA provides high legal certainty and uniformity for the stablecoin market within the EU, reducing the complexity of cross-border operations. Its strict reserve requirements for “significant stablecoins” (at least 60% of reserves held in EU-regulated banks) aim to ensure financial stability and enhance regulators’ control over large issuers. Transparency, audit, and whitepaper obligations also help protect investors.

Highlights: Direct Impact on Non-Compliant Stablecoins

One of MiCA’s most notable and direct impacts is the requirement to delist stablecoins without licenses (such as USDT). Many leading exchanges have already begun delisting USDT in the European region to comply with MiCA, directly weakening USDT’s market share and influence in the EU. This measure underscores the EU’s high priority on market compliance and may encourage more stablecoin issuers to choose compliant paths or launch euro-backed stablecoins that meet MiCA standards (e.g., Circle’s EURC), although their market size remains small for now.

Challenges and Impacts

While aiming for stability, the requirement to hold most reserves in EU banks raises concerns about potential systemic risks to the European banking system should a major stablecoin issuer encounter difficulties.

3. Hong Kong Stablecoin Regulation: Pragmatic Innovation and International Positioning

Advantages

Hong Kong’s stablecoin regulation aims to enhance the market’s standardization and security through a licensing system, high capital thresholds (minimum paid-up capital of HKD 25 million for non-bank institutions), and strict reserve requirements. It emphasizes independent reserve asset portfolios and regular audits, effectively safeguarding user funds.

Highlights: Diversified Pegging Options and Exploration of Application Scenarios

The regulation allows licensed issuers to choose different fiat currencies as the peg and requires issuers to propose specific commercial use cases. For example, JD.com’s stablecoin tests cover diverse scenarios such as cross-border payments, investment trading, and retail payments. This reflects Hong Kong’s pragmatic and open attitude towards stablecoin development, aiming to integrate stablecoins more into the real economy, especially for B2B scenarios like cross-border payments and transactions, while creating conditions for future RMB internationalization. Mainland internet giants like Ant Group actively participate in sandbox testing, confirming industry recognition of Hong Kong’s regulatory approach. On June 17, JD.com’s Liu Qiangdong stated that JD.com hopes to apply for stablecoin licenses in all major currency countries worldwide and use stablecoin licenses to achieve global corporate foreign exchange, reducing global cross-border payment costs by 90% and improving efficiency to within 10 seconds.

Challenges and Impacts

The relatively high capital and compliance requirements may pose challenges for small enterprises, leading to increased market concentration where only large institutions with sufficient resources can issue stablecoins. Additionally, it is worth noting that the current market pays more attention to stablecoin payment concepts in the Hong Kong stock market (and even the A-share market) rather than purely “crypto circle” related activities. This reflects Hong Kong’s greater focus on integrating digital assets with traditional finance and the real economy. This move aims to seize an international regulatory advantage in stablecoins, expected to attract high-quality global stablecoin projects and further consolidate Hong Kong’s position as a virtual asset hub.

2. Stablecoin Market Share & Issuer Business Models in 2025

As of July 2025, the total market capitalization of stablecoins exceeds $250 billion, with over 90% pegged to U.S. dollar assets, indicating that most stablecoins rely on the dollar as their value anchor. Additionally, according to a Deutsche Bank report, the total on-chain settlement volume of stablecoins in 2025 has reached $28 trillion, surpassing the transaction volumes of Visa and Mastercard.

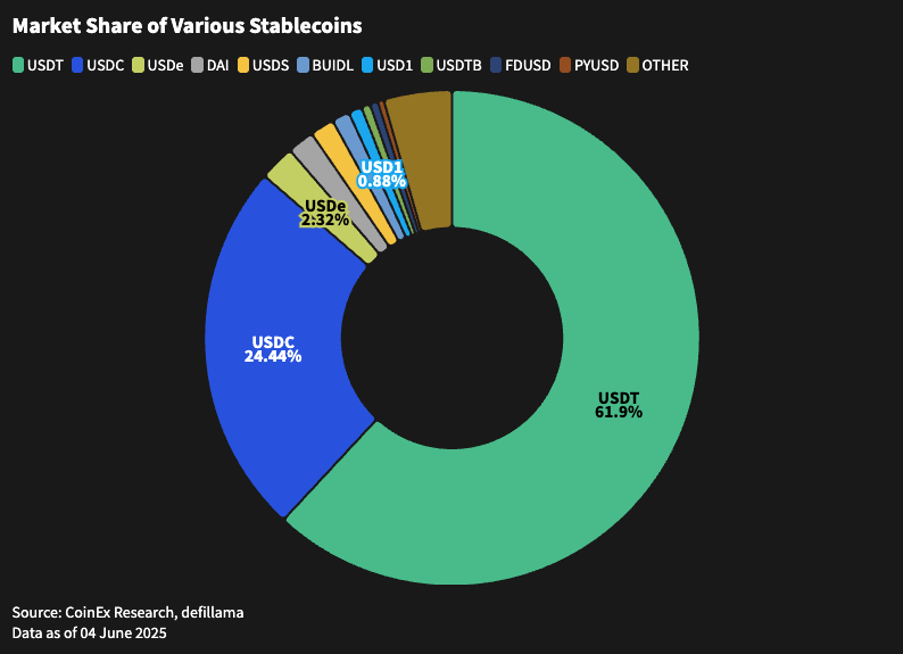

Among them, USDT and USDC are undoubtedly the dominant forces, together accounting for more than 80% of the market share. USD1, as an emerging player, has a market capitalization of only $2.2 billion, but its unique issuance background provides it with potential growth space. Overall, the stablecoin market is developing toward a larger scale.

- Technology Roadmap:

- Financial institutions (e.g., JPMorgan Chase) lean toward private blockchains (Quorum), while retail giants (e.g., Amazon) rely on cloud services (AWS Blockchain).

- Hong Kong enterprises (e.g., JD.com, ZA Bank) prioritize compatibility with the Ethereum ecosystem to integrate with DeFi.

- Compliance Strategy:

- U.S. enterprises must meet bank-level requirements under the STABLE Act, while Hong Kong enterprises rely on sandbox mechanisms for gradual compliance.

- Application Scenarios:

- Payment giants (e.g., Ant Group) focus on C-end cross-border remittances, retail giants (e.g., Walmart) target closed-loop payments within their ecosystems, and banks (e.g., JPMorgan Chase) serve B-end large-scale settlements.

- Reserve Model:

- Excluding algorithm-based stablecoins, which are banned, enterprises universally adopt 100% fiat currency or short-term bond collateral, with some (e.g., ZA Bank) adding insurance for enhanced credibility.

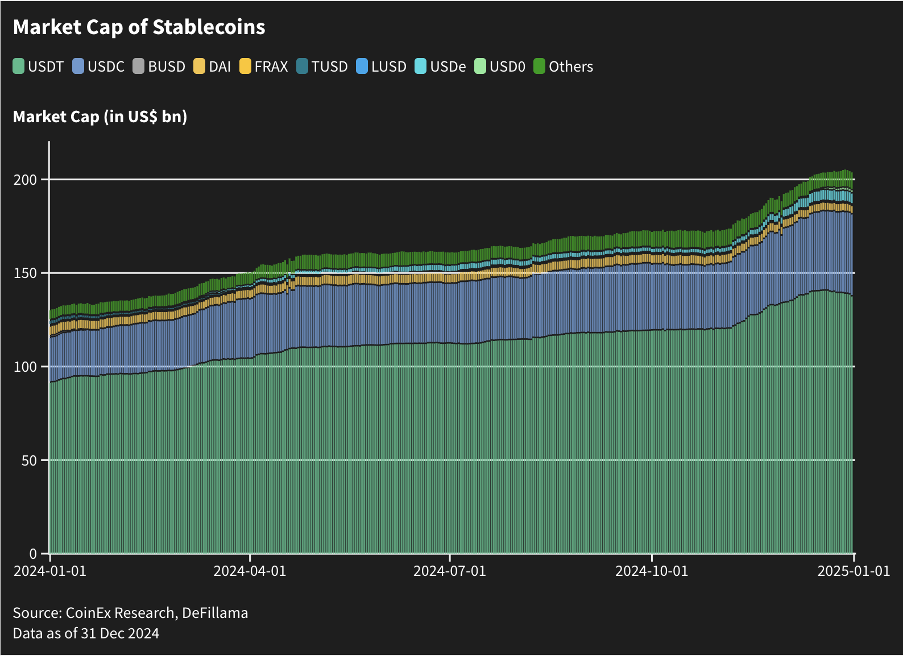

4. Stablecoin Market Structure & Related Data

4.1 Stablecoin Market Structure:

- As of June 4, the total issuance scale of stablecoins exceeded $250 billion, with over 250 types of stablecoins in existence. The market exhibits a pattern of one dominant player, one strong contender, and a flourishing diversity.

- Fully Fiat-backed: The dominant player is USDT, with a scale exceeding $150 billion; the strong contender is USDC, with a scale surpassing $60 billion. Both are off-chain stablecoins, collectively accounting for nearly 87% of the market share.

- Structured/Synthetic-backed: USDe (minted by depositing cryptocurrencies into the Ethena protocol in exchange for an equivalent stablecoin, while simultaneously establishing perpetual short contracts on CEX exchanges that never close to hedge against price fluctuations of reserve assets).

- Overcollateralized Crypto-backed:DAI, and USDS (issued on the basis of DAI via the Sky protocol, with the two being redeemable at a 1:1 ratio).

4.2 Market Share of Various Stablecoins

Changes in Market Capitalization of Various Stablecoins

5. Opportunities and Risks in Stablecoin Adoption and Yield Models

5.1 Stablecoin Issuance: The “Chicken or Egg” Dilemma and Opportunities in Interest-Bearing Models

1:1 pegged stablecoins differ from decentralized stablecoins, primarily focusing on functionality, that is, utility value. To compete with native stablecoins, they need to offer compelling use cases to attract users to switch (e.g., USDT as an exchange trading pair, USDC as an on-off ramp tool). This requires addressing why users would abandon mainstream stablecoins like USDT, necessitating unique scenarios such as USD1’s MEME Launch or partnerships with Binance for trading pairs. Additionally, providing annualized returns through channels is key, a natural advantage for interest-bearing stablecoins. Furthermore, as the variety of stablecoins increases, users face more choices. The more people use a stablecoin, the more its channels grow, but only when major channels are established will user adoption increase—this problem is inherently cyclical.

5.2 Localization Challenges: Fiat-Crypto Conversion and Payment Sector Opportunities

The primary application scenario for stablecoins is payments, and all stablecoin issuers face a common challenge: integrating actual payment functionality while navigating compliance with local financial institutions’ regulations. Currently, the adopted approach involves converting stablecoins to local currencies via on-off ramps for payment purposes. If players from the Web2 payment sector, such as Visa and Mastercard, enter the market, they could naturally resolve issuance and settlement processes, offering strong competitiveness. However, these two cannot bypass the on/off ramp process.

6. Stablecoin Outlook

The future of stablecoins will be defined by the depth of their application in payment scenarios, with the participation of large corporations and traditional financial institutions serving as key drivers for growth and maturity. As the market continues to evolve, stablecoins are expected to become an indispensable part of the global payment system, with their market potential far from fully realized.

6.1 Payment Scenarios: The Growth Ceiling for Stablecoins

The future development of stablecoins heavily depends on their use in payment scenarios, especially in cross-border payments, institutional transfers, and retail payments. USDT, as a “shadow dollar,” leverages its value anchoring advantage in OTC and exchanges to form a strong network effect, covering markets that compliant stablecoins have yet to reach, and has established a comprehensive layout in compliance, fund inflows/outflows, and payments. USDC, with stronger compliance, focuses on providing stable fund inflow and outflow services.

6.2 Large Corporation Participation: Accelerating Market Explosion

The entry of large companies and traditional financial institutions is a critical factor driving further development of the stablecoin market. For example, PayPal’s attempts and the involvement of players like Facebook, X, Alibaba, and JD.com not only enhance the credibility and stability of the stablecoin market but also potentially attract a large number of new users beyond the existing crypto community. This participation is expected to trigger explosive market growth, particularly in payment scenarios.

6.3 Other Types of Stablecoins: Niche Segments with Potential

Stablecoins remain a blue ocean but primarily for major players; traditional companies with strong channels naturally have a competitive edge, while crypto-native companies need to focus on niche segments. Although USDT and USDC dominate the market, decentralized stablecoins (like DAI) and yield-bearing stablecoins (like Ethena) may still occupy a small part of the market. These stablecoins attract specific user groups due to their unique mechanisms (such as decentralization or yield provision), but their market share is limited due to compression of basis and arbitrage opportunities after large capital inflows.

6.4 Long-Term Trend: Decoupling from Crypto Cycles, Regulation Driving Mainstream Adoption

The stablecoin market is gradually shifting from reliance on short-term fluctuations tied to crypto cycles toward becoming a long-term, sustainable asset class. This means more assets may flow into stablecoins rather than directly into other crypto assets. The improvement of regulatory frameworks, especially stablecoin regulations in the US and EU, will further promote mainstream adoption by providing a safer and more transparent environment for broader institutional and user participation.

About CoinEx

Established in 2017, CoinEx is an award-winning cryptocurrency exchange designed with users in mind. Since its launch by the industry-leading mining pool ViaBTC, the platform has been one of the earliest crypto exchanges to release proof-of-reserves to protect 100% of user assets. CoinEx provides over 1400 coins, supported by professional-grade features and services, for its 10+ million users across 200+ countries and regions. CoinEx is also home to its native token, CET, incentivizing user activities while empowering its ecosystem.

To learn more about CoinEx, visit: Website | Twitter | Telegram | LinkedIn | Facebook | Instagram | YouTube

Disclaimer: This is a paid release. The statements, views and opinions expressed in this column are solely those of the content provider and do not necessarily represent those of Bitcoinist. Bitcoinist does not guarantee the accuracy or timeliness of information available in such content. Do your research and invest at your own risk.