The cryptocurrency market is showing signs of short-term relief as Bitcoin and major altcoins attempt to stabilize after weeks of sustained selling pressure. Prices have rebounded modestly across the board, easing some of the recent bearish momentum. However, sentiment remains fragile. Many analysts argue that this move fits the profile of a relief rally rather than the start of a durable trend reversal, pointing to still-weak market structure and unresolved macro and regulatory risks.

Against this backdrop, a draft market structure bill released by the US Senate is drawing significant attention. The proposed framework represents a potential structural shift in how crypto assets are treated within the US financial system.

The bill aims to clearly differentiate which crypto assets fall under the definition of commodities and which qualify as securities, while assigning regulatory oversight accordingly. Until now, the US regulatory approach has largely relied on enforcement actions, creating uncertainty for investors, developers, and institutions alike. By outlining classification criteria in advance, the proposal seeks to reduce ambiguity and provide a cleaner operating environment.

As markets digest this information, the focus is shifting from headline-driven volatility toward longer-term structural implications. Whether this regulatory clarity translates into sustained confidence remains an open question.

A report from XWIN Research Japan highlights a critical nuance in the latest US market structure proposal: fully decentralized networks and DeFi protocols are not treated as traditional financial intermediaries. Developers, validators, and node operators are not automatically classified as regulated entities, signaling a formal recognition of decentralization as a core structural attribute rather than a loophole to be closed.

This distinction is meaningful, as it reduces legal uncertainty for open-source contributors and preserves the permissionless nature of decentralized infrastructure.

In contrast, centralized entities face a more clearly defined regulatory perimeter. Exchanges, brokers, and custodians are expected to comply with stricter rules on registration, asset segregation, and disclosure. Rather than targeting innovation, these requirements appear designed to professionalize market infrastructure and align centralized crypto businesses with existing financial standards.

Within this framework, Bitcoin, Ethereum, stablecoins, and spot ETFs are implicitly assumed to remain integrated into the US financial system, reinforcing their status as legitimate financial instruments.

On-chain data already reflects this transition. Metrics from CryptoQuant show that near the $90,000 Bitcoin level, retail activity remains muted while mid- and large-sized spot orders dominate. This pattern suggests neither speculative excess nor panic-driven exits, but measured positioning by larger investors.

Taken together, these signals imply a market gradually shifting from reactive, headline-driven behavior toward a more structure-driven phase. Regulatory clarity may not spark immediate price moves, but it is already influencing how capital positions itself across the crypto landscape.

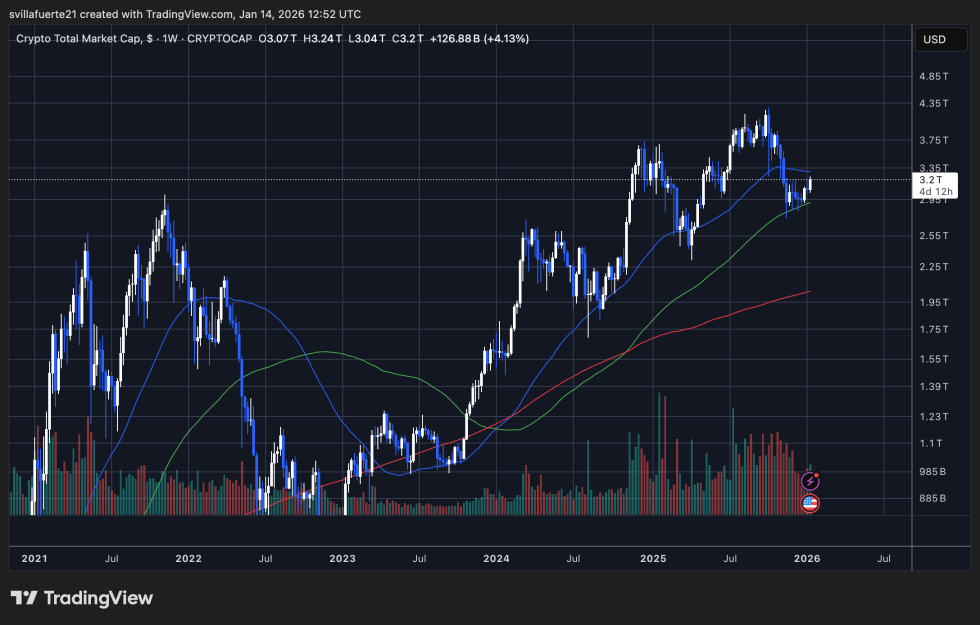

The total cryptocurrency market capitalization chart shows a market in consolidation after an aggressive multi-quarter expansion. Following the strong advance from late 2023 into mid-2025, total market cap peaked near the $3.8–$4.0 trillion zone before entering a corrective phase. Since then, price action has transitioned into a broad range, with higher volatility compressing into a more orderly structure.

Currently, the total market cap is hovering around the $3.2 trillion level, which aligns with a key former resistance zone that has now acted as support multiple times. The weekly structure suggests a cooling phase rather than a breakdown. Price remains above the rising 200-week moving average, which continues to slope upward and reinforces the idea that the primary market trend is still constructive.

Shorter-term moving averages have flattened, reflecting indecision and reduced momentum after the earlier impulsive move. Volume has declined from peak levels, indicating that aggressive distribution pressure has eased, but strong expansion demand has not yet returned. This combination is typical of mid-cycle consolidation rather than terminal weakness.

From a structural perspective, the market is digesting prior gains while maintaining a higher-low framework relative to previous cycles. A sustained hold above the $3.0 trillion region keeps the broader bullish structure intact. However, failure to defend this zone would expose the market to deeper retracements toward long-term trend support.

Featured image from ChatGPT, chart from TradingView.com