The Office of the Comptroller of the Currency (OCC) has been pressured to turn down Sony Bank’s bid to enter US crypto banking. According to reports, letters from banking and community groups filed in early November have raised sharp opposition about the plan and its possible effects.

Sony’s Bank Plan

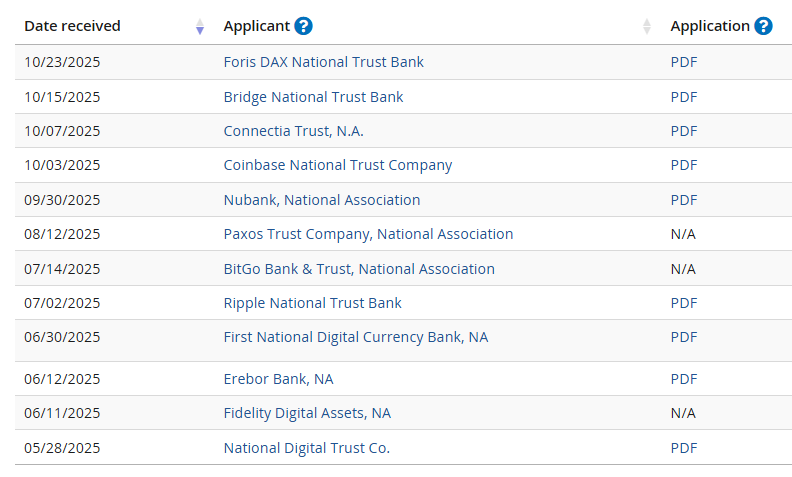

Sony Bank filed to form a national trust bank called Connectia Trust, according to filings and public reports. The plan would allow Connectia to manage reserves for a US dollar-pegged stablecoin and offer custody and asset-management services for digital tokens.

The OCC issued Interpretive Letter 1183 in March 2025, which clarified that national banks may perform certain crypto activities when they meet risk controls. Trust banks, however, do not take FDIC-insured deposits, and that difference is central to the debate.

Advocates say the structure fits within the narrow scope the OCC laid out in Letter 1183. Critics say it does not.

Source: OCC

Questions include how reserves would be composed, how redemptions would work in stress, and what would happen to custody holdings if the trust were placed into receivership.

Community bank groups and consumer advocates want clearer, more public explanations of those mechanics.

Banking Groups Push Back

On November 6, 2025, the Independent Community Bankers of America (ICBA) sent a formal letter urging the OCC to reject the application.

ICBA’s main point is that a trust charter could let a large corporate owner offer a product that looks like a deposit but lacks deposit insurance and typical bank obligations.

They called this a form of regulatory arbitrage and warned it could create unfair competition for smaller banks. The National Community Reinvestment Coalition also filed opposition, arguing the OCC lacks authority to treat a stablecoin issuer like a traditional bank and calling for stronger consumer protections.

Those groups have focused on three practical concerns: consumer confusion about what is and is not insured, unclear reserve transparency, and the lack of tested tools to resolve a trust bank that holds crypto assets.

The letters stress the potential consequences of a run on a large stablecoin and the difficulty of unwinding token custody in a crisis.

Image: Saiga NAK

Systemic And Consumer Risks

If a federally chartered trust issues a widely used stablecoin, it could set a legal precedent that other tech firms or financial firms might follow.

That is why some filings argue the OCC should move slowly and demand stricter conditions. Reports have disclosed worries that retail users could treat the token like a bank deposit, when it would not carry FDIC protection.

The risks are not just theoretical. Under stress, reserve assets might be sold quickly, and digital holdings could be hard to transfer within a receivership framework that was built for traditional assets.

Featured image from Wikimedia Commons, chart from TradingView