Most blockchains are decentralized by design. This means the nodes and stakeholders that operate and govern the platform are not concentrated as a single controlling power but instead distributed over numerous self-sovereign actors. This makes them extremely resilient to censorship while ensuring redundancy and resistance against majority attacks.

But although decentralization is a central tenet in the blockchain space and is one of the key reasons blockchains are generally considered to be ideal infrastructure for financial applications, governments, the term has lost a great deal of weight over the past decade — largely due to the advent of pools.

In case you’re not aware, mining pools are services that allow users to pool their mining resources together to increase the consistency of earning block rewards. After all, it can take small-scale miners months or potentially even years to earn a block reward while mining solo. Popular mining pools like Slushpool and F2pool combine the hash rate of all of their users together to produce a single entity that is able to more successfully mine blocks and earn rewards — which are then distributed proportionally to all its users based on their hash rate contribution.

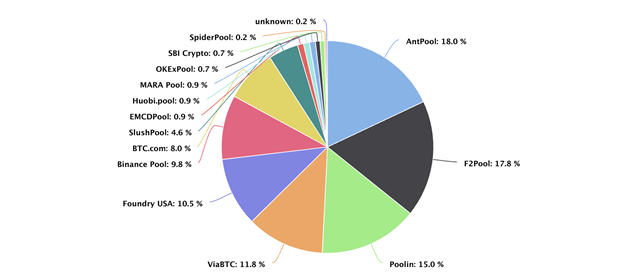

Image courtesy: BTC.com

This practice has also driven up the costs that come with successfully operating solo since individual miners generally cannot compete with pools unless they are packing potentially millions of dollars worth of specialist mining hardware. On the other hand, in Bitcoin’s earliest days, miners could be successful by simply running their mining client on their regular PC or laptop.

Nowadays, more than half of the Bitcoin hashrate is controlled by three pools (AntPool, F2Pool, and Poolin), whereas a single pool (Sparkpool) controls more than a quarter of the Ethereum hashrate. This does not align with Satoshi’s vision for a truly decentralized, community-governed payment system.

While the cryptocurrency mining arms race continues to increased centralization on major chains, this is having another knock-on effect — the risk of a 51% attack is rising. While major blockchains like Bitcoin and Ethereum are still likely immune to a 51%, the same cannot necessarily be said for smaller Proof-of-Work (POW) chains. This includes Ethereum Classic, which has suffered multiple attacks in recent years by groups that were able to seize majority control over the hashrate through rented mining power.

As a result, while increasing the overall hashrate would arguably increase the overall security of the network, this isn’t necessarily the case if this hashrate is concentrated, or if the barrier the entry is so high that the number of individual participants dwindles.

But while decentralization is a necessary characteristic of any successful blockchain, the competition that the Proof-of-Work (POW) consensus mechanism induces isn’t. Instead, blockchains need a fair, non-competitive means to achieve decentralization while still rewarding those that help operate and secure the network.

This is exactly what Minima — a lightweight blockchain designed to power a truly democratic DApp ecosystem — looks to achieve. Unlike most other blockchains, every user on the Minima network operates as a full node and helps to contribute to the maintenance of the network. In return, they receive a reward.

If you loved #bitcoin, wait til you get a load of what we're building. It's what we meant for bitcoin originally. True #decentralization. Not a group of centralized mining farms in control 👍🏽 https://t.co/R1180lEg7O

— Minima (@Minima_Global) September 16, 2021

Unlike other platforms, every participant on the network is equal (there is no stratification by hashrate), and the barrier to entry is extremely low — since the software even runs on mobile devices. With this feature, Minima hopes to deliver the capabilities of decentralized applications to the masses, without diluting the power of the individual.

With decentralization increasingly coming into focus as something that must be carefully preserved with the growth of any blockchain system, there is a good chance that major blockchains like Bitcoin, Ethereum, Binance Smart Chain, and more will need to implement policies that enforce this to ensure continued success.