Bitcoin has recently been rising in the midst of widespread banking sector issues, prompted by Silicon Valley Bank.

But bank runs have been a recurring issue throughout history, causing significant damage to the economy.

The collapse of major banks and the panic that followed during the Great Depression of the 1930s led to the creation of regulatory bodies such as the Federal Deposit Insurance Corporation (FDIC) to prevent future crises.

While the banking industry has evolved significantly since then, with the rise of online banks and fintech companies, the potential for crises still exists. Recent events show this risk is very real, prompting many to look to Bitcoin as a solution to avoiding banking crises.

In this article, we will explore the history of bank runs, their impact on the economy, and the measures taken to prevent them. We will examine examples of bank runs throughout history, including the Savings and Loan Crisis of the 1980s and the 2008 Financial Crisis.

Additionally, we will discuss the rise of alternative banking methods such as online banks and fintech companies, and the potential for future crises in the face of economic uncertainty.

Finally, we will examine the role of Bitcoin as a decentralized, borderless alternative to traditional banking methods, and its potential in preventing future bank runs.

The Great Depression and the Birth of Bank Runs

The Great Depression of the 1930s is one of the most significant events in the history of bank runs.

The stock market crash of 1929 triggered a wave of panic and uncertainty, leading to the collapse of many major banks.

People rushed to withdraw their savings from banks, fearing that their deposits would be lost forever.

The Collapse of Major Banks and the Panic that Followed

As banks struggled to meet the demands of customers, many failed to provide their promised payouts.

This further fueled panic, causing people to withdraw their money from other banks as well. This vicious cycle created a domino effect, with banks failing one after another.

Customers who were not able to withdraw their money from these banks were left with no savings or financial security.

The Role of Government Intervention and the Creation of the FDIC

The Great Depression prompted the U.S. government to intervene in the banking system.

In 1933, the Federal Deposit Insurance Corporation (FDIC) was created to insure bank deposits and prevent future bank runs.

This guaranteed customers that their deposits would be safe up to a certain amount, restoring their confidence in the banking system.

The FDIC’s creation was a significant turning point in the history of bank runs. It created a safety net for customers, ensuring that they would not lose their savings even if a bank were to fail.

This provided the public with much-needed reassurance, stabilizing the banking system and preventing future runs.

Bank Runs in the 20th Century

The 20th century saw the rise of electronic transfers and the advent of modern banking.

While bank runs continued to occur, they took on a different form in the face of technological advancements.

Here are some examples of bank runs in the 20th century and how they differed from those in the past.

The Impact of Technology on Banking

The rise of electronic transfers made it easier for customers to move their money around. While this made banking more convenient, it also made it easier for bank runs to occur.

For example, in 1996, rumors of financial instability led to a bank run on Britain’s oldest building society, the Bradford & Bingley. Customers were able to withdraw their savings quickly and easily, contributing to the bank’s eventual collapse.

The Savings and Loan Crisis of the 1980s

The Savings and Loan Crisis of the 1980s was a significant event in the history of bank runs. Over 1,000 banks failed during this crisis, causing panic and leading to a wave of bank runs.

The crisis was caused by a combination of factors, including high interest rates, risky investments, and deregulation of the banking industry.

This crisis prompted the government to step in and create the Resolution Trust Corporation (RTC) to manage the assets of failed banks.

The 2008 Financial Crisis

The 2008 financial crisis was another major event in the history of bank runs.

The collapse of Lehman Brothers triggered a wave of panic, causing people to withdraw their savings from banks. This led to a freeze in lending, contributing to a global economic recession.

The government’s response to the crisis was to bail out failing banks and implement new regulations to prevent future crises.

Bank Runs in the 21st Century

The 21st century has seen the rise of alternative banking methods, such as online banks and fintech companies.

While these innovations have brought many benefits, they have also created new challenges for the banking industry.

Here are some examples of bank runs in the 21st century and how they have been impacted by technological advancements.

The Rise of Alternative Banking Methods

The rise of online banks and fintech companies has made banking more convenient than ever before. Customers can easily access their accounts and transfer money using their smartphones.

However, these innovations have also created new challenges for the banking industry.

For example, in 2018, rumors of financial instability led to a bank run on online lender, Tandem Bank. Customers were able to withdraw their money quickly and easily, causing panic and leading to a temporary freeze on withdrawals.

The Impact of the COVID-19 Pandemic

The COVID-19 pandemic had a significant impact on the banking industry, causing widespread economic uncertainty and leading to a wave of bank runs.

In the early days of the pandemic, people rushed to withdraw their savings from banks, fearing that the financial system would collapse.

This led to a shortage of cash and a freeze on lending, contributing to the economic downturn.

Silicon Valley Bank and the Start of Another Crisis

Silicon Valley Bank, a prominent US-based bank that specializes in providing financial services to the technology and innovation sectors, recently experienced a bank run.

In response to rising instability concerns, some of Silicon Valley Bank’s customers reportedly began withdrawing their deposits en masse, leading to a liquidity crunch for the bank.

The Potential for Future Bank Runs

While the banking industry has become more secure and stable since the Great Depression, the potential for future bank runs still exists.

Economic uncertainty, technological advancements, and other factors can all contribute to the likelihood of bank runs.

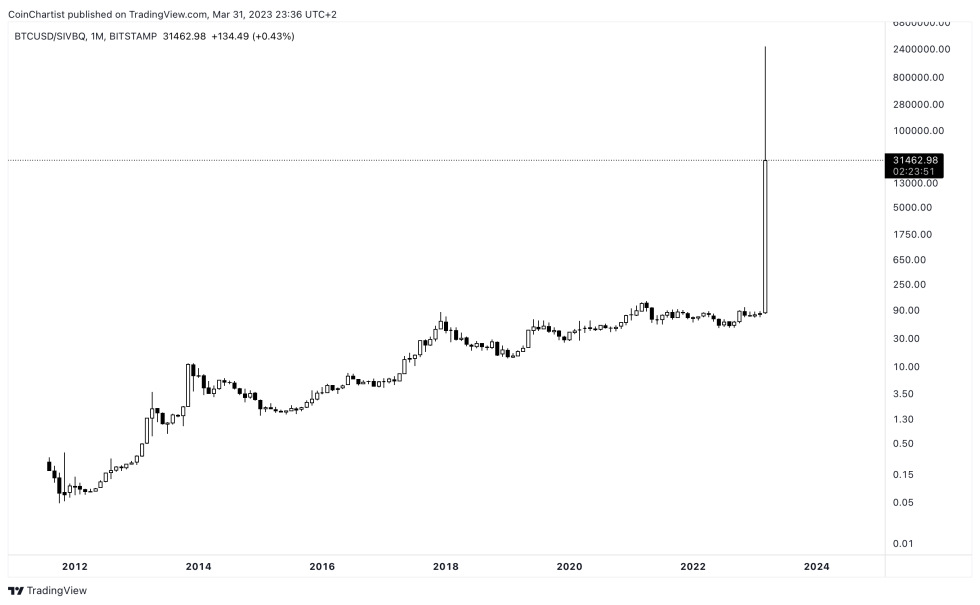

BTC priced in Silicon Valley Bank shares | BTCUSD on TradingView.com

Bitcoin as a Solution to Avoiding Banking Crises

Bitcoin, the world’s first decentralized cryptocurrency, is becoming an increasingly popular alternative to traditional banking methods.

As the financial system continues to face potential crises, more and more people are turning to Bitcoin as a way to avoid the risk of bank runs and other financial disruptions.

Origins of Bitcoin

Bitcoin was created in 2009 by an unknown person or group using the pseudonym Satoshi Nakamoto.

The first Bitcoin transaction took place in January 2009, when Nakamoto sent 10 Bitcoins to a developer named Hal Finney. The genesis block of the Bitcoin blockchain includes a headline from the UK newspaper The Times, reading “Chancellor on brink of second bailout for banks.”

This headline is believed to be a commentary on the instability of the banking system and the need for a new, decentralized solution.

Bitcoin’s Advantages in Times of Crisis

Bitcoin offers several advantages over traditional banking methods in times of crisis.

Firstly, it is decentralized, meaning that it is not controlled by any central authority or institution. This makes it less vulnerable to government intervention and economic instability.

Secondly, Bitcoin transactions are fast, secure, and can be done anonymously, making it an attractive option for those who wish to protect their financial privacy.

Finally, Bitcoin is a borderless currency, meaning that it can be used by anyone, anywhere in the world, without the need for intermediaries or government regulations.

Bitcoin’s Role in Preventing Bank Runs

Bitcoin is increasingly being seen as a way to prevent bank runs and other financial crises.

With Bitcoin, individuals can hold their own assets, rather than relying on a bank to hold their deposits.

This reduces the risk of a bank run, as individuals can withdraw their assets at any time, without the need for a central authority to approve the transaction.

This decentralization also means that the financial system is less vulnerable to economic downturns or government interventions, as Bitcoin operates independently of these factors.

Conclusion

Bank runs have been a recurring issue throughout history, causing significant damage to the economy.

The Great Depression of the 1930s marked the birth of bank runs and led to the creation of the Federal Deposit Insurance Corporation (FDIC), a turning point in the history of bank runs.

The 20th century saw the rise of electronic transfers and the advent of modern banking, leading to new challenges for the banking industry.

The 21st century has brought even more changes, with the rise of online banks and fintech companies, as well as the potential for crises like the COVID-19 pandemic.

As the banking industry continues to unravel, it is likely that Bitcoin and other cryptocurrencies will play an increasingly important role in the financial landscape.

By learning from the history of bank runs and adapting to new challenges, including the potential for decentralized cryptocurrencies like Bitcoin, we can work towards a more stable and secure financial future.