Solana co-creator Anatoly Yakovenko, in an aggressive move that could potentially reshape the fate of the embattled cryptocurrency exchange FTX and bolster the Solana network, has called for the redistribution of SOL tokens currently held in FTX’s reserves to the exchange’s former customers.

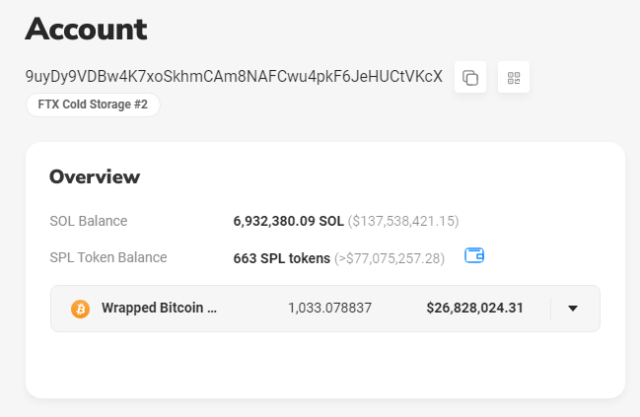

It has been revealed that FTX’s cold storage wallets, identified through the Solscan blockchain explorer, initiated the movement of their SOL holdings. These wallets collectively house approximately 7 million SOL tokens, valued at a staggering $134 million at today’s market rates.

Source: Solscan

A Dual Solution For FTX Customers And Solana Network

Yakovenko, also called Toly, on X proposed that the substantial allocation of SOL tokens to millions of new users not only serves as a means to compensate FTX customers but also presents an opportunity to enhance the Solana network’s vitality. By welcoming a wave of new participants into the Solana ecosystem, this move could stimulate growth, foster decentralization, and breathe new life into the network.

.@adamscochran if you have any influence with the ftx estate, my wish would be to distribute the sol to all the ftx customers directly. Probably the least worse outcome for everyone.

— toly 🇺🇸 (@aeyakovenko) August 31, 2023

Toly contends that this approach might prove more efficient than the protracted legal procedures FTX has been embroiled in since its bankruptcy.

The Interwoven History Of FTX And Solana

Before its precipitous downfall in November 2022, FTX had a profound symbiotic relationship with Solana, the 10th-largest cryptocurrency by market capitalization. Sam Bankman-Fried, co-founder and former CEO of FTX, was a prominent advocate for SOL, cementing their association.

SOL market cap currently at $8.10 billion. Chart: TradingView.com

Under FTX’s umbrella, a marketplace for Solana NFTs was established, alongside strategic investments in various Solana-related projects. This interconnectedness made the network especially vulnerable when FTX crumbled, causing the altcoin’s value to plummet from $260 to a mere $8 in a matter of months.

FTX’s Troubled Past And Legal Battles

The downfall of FTX, which allegedly resulted from criminal mismanagement, was a seismic event in the cryptocurrency industry. It is reported that approximately $8.7 billion in customer funds were misappropriated, resulting in a slew of criminal charges. Bankman-Fried, the former face of FTX, faced a total of 13 criminal charges following his arrest in the previous year.

The legal quagmire surrounding the exchange’s demise has left many former customers in limbo, uncertain about the fate of their assets.

Also see https://t.co/5w4sTdkviX [unlocks tab] for a schedule of all unlocks (not just FTX) pic.twitter.com/kc5OJ9qDYA

— ashpool (@solanobahn) August 31, 2023

Yakovenko’s proposal to redistribute SOL tokens from FTX’s reserves to its former customers offers a unique opportunity to rectify the damage wrought by the exchange’s collapse while simultaneously rejuvenating the Solana network.

As the cryptocurrency community watches this development closely, the potential for a win-win scenario looms large, injecting fresh optimism into both FTX customers and Solana enthusiasts.

Featured image from Entrepreneur