Why use blockchain technology? While there are certainly a lot of advantages to a distributed ledger, it may not be applicable to all companies or individuals–not yet, at least.

The second question people usually ask when they hear about blockchain is–why use blockchain? Why use a distributed ledger? Why not use a regular database or legacy system as a system of record in this already digital world?

After all, in many cases for business owners, updating existing infrastructure with blockchain technology may be costly, labor-intensive and not really worth it.

In this article, we examine what a blockchain really is, what blockchain applications are, what they can do and–most importantly–why use blockchain?

What Is Blockchain? A Distributed Ledger

Just in case you need a little catch-up, people often talk about “blockchain” in the singular, as if it were only one. In reality, they should be talking about blockchain technology (also known as Distributed Ledger Technology or DLT) or blockchains in the plural, since there are many different ones, including public (permissionless) and private (permissioned) blockchains.

Examples of public blockchains and distributed blockchain technology include the Bitcoin blockchain, the Ethereum blockchain, the NEO blockchain, and many others. Permissioned blockchains are adapted for corporate or organizational use, with one such example being IBM’s Hyperledger blockchain. But we’ll get into that in a moment.

A blockchain (or distributed ledger) is essentially a massive, ever-growing ledger in which all blockchain transactions are recorded.

Each block in the chain is chronologically connected to previous blocks and synched with the network nodes. This means that changing the data in one block would mean having to reverse all previous blocks before it, making it very hard to tamper with–very hard, although not entirely impossible.

This is true of Ethereum, Bitcoin, and any other cryptocurrency that runs on blockchain technology using the proof-of-work consensus algorithm. To get a concise sense of the nature of blockchain and what blockchain offers, check out this explainer video below:

How Blockchain Works

The data sent to each block on the distributed ledger is based on encrypted Merkle Trees, which is a technical way of saying that no fraudulent transactions can be recorded. If any transaction that does not follow protocol rules is detected by the network nodes, it is expelled immediately. This inherently secure nature of distributed blockchain technology means that it prevents damage to the entire blockchain shared database and can cut off a hacking attempt at one block.

The most well-known blockchain is that of the Bitcoin network where every transaction (that follows the protocol) is recorded and included in a block. Once a transaction is broadcasted to the network and confirmed by miners, the action cannot be reversed, nor can it be tampered with in any way. The same is true of Ethereum, which is responsible for smart contract technology.

This open-source public ledger displays a history of all transactions and transaction data ever made. Most blockchains are sustained by miners. In the case of the Bitcoin blockchain, for example, it is the job of miners to confirm a Bitcoin transaction to the rest of the Bitcoin network by including them in blocks. Ethereum transactions on the Ethereum network work in the same way.

These public blockchains are global and decentralized, visible to all. While many believe blockchains to be a system of record, they are not actually an effective means of storage, but verification. Simply put, blockchains ensure that everyone is on the same page and no single person can change the ledger for anyone else–if they did, the network would reject the attempt.

This means that when one person sends bitcoin or ETH funds to another, the transaction data is public. That doesn’t mean that your name and private data is splashed all over the web, but the public address and amount can be seen.

This is a key quality of blockchain technology that makes it so efficient when it comes to record verification and industries which require transparency. However, a decentralized public ledger where payment amounts are visible to all is not necessarily practical or useful in cases where privacy is necessary or desired.

What Blockchain Can Do

There has been a lot of marketing hype over what blockchain can do and what blockchain offers. To be sure, it is a life-changing technology that will bring great things over the years to come. But it’s also not a panacea for all the world’s ills.

The very ability to transact peer-to-peer on the distributed ledger without a trusted middleman makes blockchain technology revolutionary.

However, there have been plenty of fraudulent or over-exaggerated claims about what blockchain is for and what it can do. This is especially true through initial coin offerings where companies raise vast amounts of money often claiming to be able to use blockchain to realize their ambitious ideas. These pitches could be almost anything from transforming real estate to managing drone traffic.

So let’s set the record straight. No, it can’t cure cancer, but there may be ways in which the medical industry can incorporate the technology into their research or record verification. It may be complicated right now to purchase real estate using smart contracts on blockchains, but the potential is there once legislation catches up.

Blockchain can also give people a digital identity, which is portable and can prove who they are, removing the need for, say, a passport or social security number, which can be forged or tampered with as we’ve seen with many cases of identity theft.

Many companies and business owners are examining the use of blockchain for their business processes. Walmart, for example, traced produce around the world through the supply chain with successful results and has registered several blockchain patents indicating its interest in the technology moving forward.

The supply chain, in fact, is a great example of where blockchain technology can be particularly useful. Here, cross-border payments must be made and transaction fees are high, along with currency conversions and plenty of intermediaries taking their cuts.

Since blockchain can ensure the data is tamper-proof and immutable, the digital identity becomes indisputable. This holds enormous potential to cut out not only trusted third-parties but also corruption at different points in the supply chain.

There is also the chance for companies and individual members in the supply chain to pay using one standard cryptocurrency thus removing conversion fees while reducing transaction fees and times.

Beyond the supply chain, though, any industry that requires record-verification and transparency can benefit from blockchain–from real estate to financial services. Capital markets and venture capital have already been changed forever by the decentralized nature of blockchain technology. As has the concept of digital identity.

One of the key takeaways about public blockchain technology is that it’s decentralized, which means that it is not controlled by any single entity, a central authority or central servers. Permissioned blockchains, however, may not share all of these properties. More on that later.

Unlike typical databases or IP addresses that are controlled by one central authority, blockchain cannot be shut down because it is run across a network of nodes. This also means that it has no single point of failure and makes it more resistant to hackers than centralized ‘honeypot’ databases.

So when we return to the question of “why use blockchain?” this is an extremely important point to keep in mind. Just consider countries where censorship is a problem and the government shuts down certain pages and channels, such as China with Wikipedia or Google. With blockchain technology and a blockchain application, this would be impossible on the protocol level.

Blockchain vs Normal Databases

Here are some of the advantages that blockchain offers over a regular database or other existing technologies:

Immutability – Thanks to its Proof-of-Work system, blockchains can offer near-immutable transactions. When data decentralized on a blockchain is verified, it makes it practically impossible to roll it back and tamper with the data. This gives blockchain tech a strong use case in industries where records need to be verified and accurate, such as medical records, land deeds, birth certificates, or social security numbers.

Security – Blockchain technology is especially secure when compared to centralized databases. This means that it is much less likely to be the target of a hack as there is no one single point of failure.

If one block is hacked it will be rejected from the system and nipped in the bud before any damage is done. The more nodes and hash power the network has, the more secure it is, making the Bitcoin blockchain generally considered to be the most secure public blockchain today.

Redundancy – Using distributed blockchain technology, you have the same set of data distributed in multiple places around the world, which means that the data is extremely secure and practically impossible to lose. When you consider this type of advantage for a large and small business that have suffered data leaks and hacks, blockchain offers a huge advantage.

Cost Reduction – By using distributed blockchain technology that runs over a network of nodes, you no longer need the additional staff members to maintain a DevOps system. A small business can make significant cost savings by using blockchain technology and smart contracts to cut out middlemen for administrative tasks or financial services.

Accountability – With all of the above characteristics, businesses and individuals alike can be sure that the data is true and that no banking insurance or additional verification is needed–the digital identity of each contributor is clear. This makes it easier for companies to hold people accountable for any attempt at entering wrongful data into the system.

Can Blockchain Be Hacked?

The nature of blockchain and the words “immutable” and “secure” often raise questions over why there appear to be so many hacking attacks and scams from initial coin offerings. So, can blockchain be hacked? Well, the hacking of exchanges that we see on a common basis has nothing to do with blockchain technology but with secondary software weaknesses, such as exchanges, vulnerabilities in smart contract code, and wallet providers.

Blockchain is extremely safe when you consider its decentralized nature and the fact that a hacker or bad actor cannot enter the system easily and cause a disaster like with Equifax. Hacking a blockchain as large as the Bitcoin blockchain would require resources, power, coordination that outstrip the GDPs of many small countries.

But, it is possible for blockchains to be hacked. In what is called a 51% attack, a hacker needs to gain control of the majority of the network mining hash power. With smaller, permissioned blockchains, a hack is easier to pull off, but with a network such as the Bitcoin, this is almost impossible. The Bitcoin blockchain is the most resistant to this type of attack today.

On a more complex network such as the Ethereum network, the attack surface is potentially bigger. Ethereum actually underwent a hacking attack in 2016 called the DAO hack, which was caused not by a 51% attack, but by a loophole in a smart contract.

This saw Ethereum split into two, between those who believed that “code is law” and those who wanted to safeguard the future of Ethereum by initiating a hard fork to essentially roll back the damage that had been done.

This lead to the creation of Ethereum Classic as a separate cryptocurrency was derived from the code override.

Permissioned Blockchains vs Public Blockchains

Public blockchains allow anyone to take part and are visible to all. The Ethereum blockchain, in particular, has a very strong community of developers who create their own decentralized application, otherwise known as a “DApp.”

This type of decentralized application strengthens the Ethereum network and means that more people add to its creativity and security. Perhaps one of the most memorable to date was CryptoKitties. This decentralized application congested the Ethereum blockchain (causing transaction fees to soar) as the demand was so high yet at the same time, drew more people to the network.

The Bitcoin blockchain, too, has more people auditing, reading, writing code for it and mining than many other blockchains.

With permissioned blockchains (also called private blockchains) the exact opposite is true. The only people auditing and transacting on the blockchain are the ones given the classification and access to do so.

There is a central entity and the actions can be deleted and overridden, which makes sense for corporations, or a large or small business that needs control. However, this flies in the face of blockchain’s “immutability” claim.

Immutability does not apply to permissioned blockchains, and as such, they are more vulnerable to hacking than a public blockchain.

The benefits of permissioned blockchains are obvious in that they can keep certain classified information secure, and they are much faster than public blockchains. The number of people on them doesn’t require thousands of nodes and their consensus to run since the validating nodes are typically selected by the central entity.

Blockchain vs Cryptocurrency

It’s easy to confuse blockchain with cryptocurrencies and in fact, they are really two different sides of the same (virtual) coin. Many people make the distinction as Bitcoin, Ethereum, or Bitcoin Cash being the digital currency and blockchain the technology that runs underneath them. However, the separation is somewhat arbitrary.

Cryptocurrencies are digital assets in which the value is transferred peer-to-peer with no need for centralized authorities or trust. There are currently more than 2,000 cryptocurrencies available and not all are created equal. The main types of digital currency are Bitcoin, Ethereum, Ripple, Bitcoin Cash, Litecoin, and Steller Lumens… but the list is long.

Cryptocurrencies allowed for the rise of initial coin offerings, a peer-to-peer way of raising startup funds that eclipsed venture capital funding in early innovation last year.

Recently the Ethereum price dropped sharply, taking it from its position as the second largest cryptocurrency by market cap, to the third, beaten in market cap by XRP. Ethereum price, Bitcoin price, and all major cryptocurrency prices have taken a tumble recently, proving how sensitive they are to outside speculation and external market pressures.

Cryptocurrency isn’t widely accepted yet, although there have been cases of people selling their houses and real estate developments for bitcoin, such as the Aston Plaza in Dubai.

The blockchain, on the other hand, lies underneath the digital assets that regularly updates the state of the network, i.e. balances. This cuts out the need for a middleman and essentially for a bank or bank insurance.

Cryptocurrencies are really just a subset of the broader range of applicabilities of blockchain technologies. While many people try to separate cryptocurrencies from blockchain, tarnishing cryptocurrency as a tool for criminals while painting blockchain as a respectable technology, is disingenuous in many ways.

What really gives rise to all these opportunities in any industrial sector is the notion of the smart contract and its decentralized computation. Which brings us to our next question…

What Are Smart Contracts?

Smart contracts are automated agreements that allow us to transfer money, data, property deeds, shares, or anything else of value in a transparent way. Many people believe that smart contracts were invented by the Ethereum network, however, the American computer scientist who invented BitGold in 1994, Nick Szabo, first came up with the concept.

Smart contracts are a game changer in the blockchain world since they allow us to cut out the intermediaries. They are set up between two or more parties and self-execute based on a set of predetermined conditions.

When it comes to making a trade, for example, traditionally you would need to pay a broker to do it for you. With smart contracts, you simply load your escrow with cryptocurrency and carry out the trade.

If you want to make a Bitcoin transaction or Ethereum transaction, for example, from one person to another, you can automate it in a smart contract. The Bitcoin price or Ethereum price that you agree upon according to the terms of the smart contract cannot then be changed or altered and the funds cannot be reversed once sent.

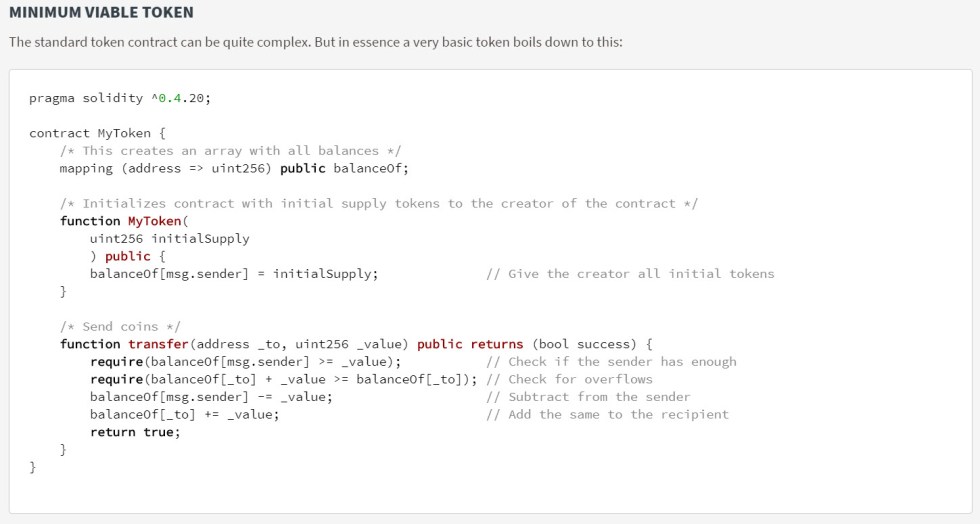

Below, you can check out the code for the most basic smart contract written on the Ethereum blockchain. While smart contracts can be encoded for all blockchains, Ethereum allows for unlimited processing capability.

What is Bitcoin Mining?

Bitcoin mining is where computational power is spent to confirm Bitcoin transactions and to introduce new bitcoins to the system. The same is true of Ethereum mining. Cryptocurrency mining is intentionally designed to be resource intensive through its Proof-of-Work (PoW) model. Though many bitcoin mining farms are incentivized to seek cheaper and renewable energy sources. Meanwhile, Ethereum mining is looking to switch to a Proof-of-Stake (PoS) model in the future, which would require fewer resources compared to PoW.

Bitcoin mining requires miners to solve complex mathematical equations to confirm transactions and prevent the problem of double-spending. For their efforts, Bitcoin miners are rewarded. The current reward for Bitcoin mining is 12.5 bitcoin for every block found (about 1,800 bitcoins a day), though this amount is expected to decrease over time (since the amount of bitcoins that will ever exist is fixed at 21 million).

Mining today requires complex machinery and high operational costs. This Bitcoin mining is now largely centered in large mining corporations since individuals can no longer mine from their home PCs given the increasing difficulty and high Bitcoin price.

Is Blockchain Legal?

One question that appears a lot is whether or not blockchain is legal. Regulatory compliance seems to be an issue that varies from jurisdiction to jurisdiction. However, since countries like China banned initial coin offerings and the use of cryptocurrency, that does not mean that blockchain technology needs to achieve regulatory compliance. Like the internet, blockchain is a technology and cannot be regulated on the protocol level.

Countries are concerned about regulatory compliance due to the explosion of raising funds on the blockchain since there have been plenty of scams leaving uninformed investors out of pocket. Exchanges and cryptocurrency wallet providers should also achieve regulatory compliance, so as to protect their users in the case of a hack. Social security is important to countries and they need to ensure their citizens are well-informed or protected from investing in scams.

While some jurisdictions implement KYC as a minimum requirement for regulatory compliance, this is not helpful when it comes to an external breach, such as a hack.

Who Created Blockchain?

Satoshi Nakamoto created the Bitcoin blockchain although the foundations for the technology had been laid down long beforehand. Satoshi Nakamoto is, in fact, a pseudonym and the author of the Bitcoin whitepaper that appeared in 2008.

Many people say that Bitcoin came about a response to financial institutions and capital markets over the banking crisis of that year. It seems that Satoshi Nakamoto intended Bitcoin to be a decentralized peer-to-peer currency for borderless frictionless payments that cut out all trusted middlemen (that historically cannot be trusted, i.e. central banks). Beyond digital relationships, people can transfer more than just data–they can transfer value as well.

In fact, blockchain has often been referred to as the “internet of value,” since people can send digital currency to each other without a central authority and simply using a private key to access the funds from anywhere on earth.

No one truly knows who Satoshi Nakamoto is although most believe that this is one major advantage of Bitcoin since it allows people to concentrate on the work at hand and the technology.

Wrapping It Up – Why Use a Blockchain?

Blockchain technology and its public ledger is still in its infancy although there are many reasons certain companies, financial institutions, and even governments may eventually want to incorporate it. The technology offers security, potential cost reduction, and infinite possibilities for supply chain management while cutting out many intermediaries.

As we’ve seen, apart from in extremely rare circumstances, blockchains are certainly more censorship-resistant and tamper-proof than legacy databases. Governments or non-profits may also use blockchain technology if they want to verify the information is accurate and true, such as with voting, or medical records. They have plenty of reasons to consider the question of “why use a blockchain?”

Financial institutions are already using blockchain technology to speed up cross-border payments and reduce transaction fees. And we’re seeing more and more use cases for what the technology offers every day, including blockchain technology in the energy industry. However, while it remains in its early stages, small companies may not wish to hop on the blockchain bandwagon just yet.

Why use a blockchain? Why use any technology? Because it speeds up processes, improves efficiency and lowers cost. If blockchain technology or any other application platform doesn’t yet do that for your company, it isn’t worth it yet.