A new policy brief, published by the Bitcoin Policy Institute (BPI), lays out an ambitious plan to transform US government debt management by embedding Bitcoin purchases directly into Treasury bonds. Authored by Andrew Hohns, PhD, and Matthew Pines, the paper, titled “Bitcoin-Enhanced Treasury Bonds: An Idea Whose Time Has Come,” proposes issuing up to $2 trillion in so-called “₿ Bonds”—with 10% of bond proceeds dedicated to acquiring $200 billion in Bitcoin for a government-held Strategic Bitcoin Reserve (SBR).

“The United States faces an unprecedented fiscal challenge with approximately $9 trillion of federal debt maturing within the next twelve months, and over $14 trillion within the next three years,” the authors write, arguing that elevated market interest rates near 4.5% impose “significant ongoing costs to service this debt.”

Under the proposal, the US Treasury would roll out a specially structured sovereign instrument—referred to interchangeably as “₿ Bonds” or “BitBonds”—that pays 1% in annual coupon interest (compared to the current 10-year Treasury rate of around 4.5%). While 90% of each bond’s proceeds go toward the usual government funding channels, the remaining 10% is allocated to BTC acquisition.

That BTC would be deposited in the SBR, a federal asset pool set in motion by President Donald Trump’s March 6, 2025 Executive Order which designates Bitcoin as “digital gold” and directs federal agencies to develop “budget-neutral strategies for acquiring additional Bitcoin without imposing costs on American taxpayers.”

Reducing Debt Costs And Building A Bitcoin Reserves

Citing existing Treasury data, the paper calculates that replacing a portion of traditional refinancings—up to $2 trillion—with these low-coupon ₿ Bonds could generate substantial savings. By cutting the coupon from 4.5% to 1%, the authors estimate the government could save $70 billion per year, or $700 billion over ten years, with a present value they peg at around $554.4 billion.

“After accounting for the initial BTC purchase of $200 billion, the program delivers net taxpayer savings of $354.4 billion even if Bitcoin prices remain static,” the brief explains.

Crucially, bondholders would receive their principal (backed by the full faith and credit of the US government) and a guaranteed interest rate—albeit a low one—and also a variable bitcoin-linked payout at maturity. The mechanism hinges on the Bitcoin portion generating upside to compensate for the lower coupon. Investors get full principal protection, while any BTC appreciation is shared between the government and bondholders. According to the brief, “This structure ensures that investors receive their full principal plus interest at maturity regardless of bitcoin’s price performance.”

A key talking point in the proposal is the potential for extraordinary gains if Bitcoin’s historical growth rates persist. The authors present a range of scenarios where the Bitcoin allocated for each ₿ Bond appreciates over time. At a 30% compound annual growth rate, the government’s share of the upside in the SBR might exceed $0.83 trillion in a decade. More optimistic projections reach into the tens of trillions of dollars in value. While acknowledging volatility risks, the brief notes that “longer holding periods (greater than four years) have consistently delivered positive returns” based on historical data.

In an effort to entice American households, the authors advocate conferring tax-free status on both the bonds’ coupon payments and the Bitcoin-linked gains, provided holders keep the bonds to maturity. “The combination of principal protection, potential BTC upside, and tax advantages would make ₿ Bonds particularly attractive to middle-class families,” the paper reads. This provision aims to “democratize access to bitcoin’s growth potential within a safe, familiar investment vehicle.”

Phased Implementation Roadmap

The policy brief lays out a three-phase approach:

- Pilot Program (3–6 months): A small-scale rollout of $5–10 billion in ₿ Bonds under existing executive authority, testing investor demand and establishing secure custody measures.

- Policy Development and Expansion (6–12 months): Formal legislation, broader market issuance, and regulatory guidance from Treasury, Congress, and agencies such as the SEC or CFTC.

- Full Implementation (12–24 months): Incorporating ₿ Bonds as a standard Treasury offering, potentially covering up to 20% of total federal refinancing needs over the next three years.

Critics might question whether introducing a volatile asset like Bitcoin into sovereign debt raises exposure to price swings. The authors counter that “the program limits Bitcoin allocation to 10% of bond proceeds, containing the impact of potential volatility.” They also propose employing robust multi-signature custody, cold storage for large reserves, and security audits for operational resilience.

In terms of international and domestic buy-in, the BPI’s report points to new classes of investors—both retail and institutional—who may welcome a US-backed instrument that includes Bitcoin returns. It also stresses foreign investor interest: some sovereign wealth funds and central banks might be drawn to a hybrid debt instrument offering partial exposure to digital assets, though the brief acknowledges the need for diplomacy and coordination with global financial institutions.

Ultimately, the “Bitcoin-Enhanced Treasury Bonds” white paper frames this effort as a proactive response to $14 trillion in upcoming federal debt maturities, attempting to transform the government’s refinancing burden into a strategic opportunity. “₿ Bonds are a win-win-win,” the authors conclude, “lower interest rates on the 10-year, revenue-neutral to revenue-positive growth of the SBR, and exceptional tax-advantaged returns for US investors.”

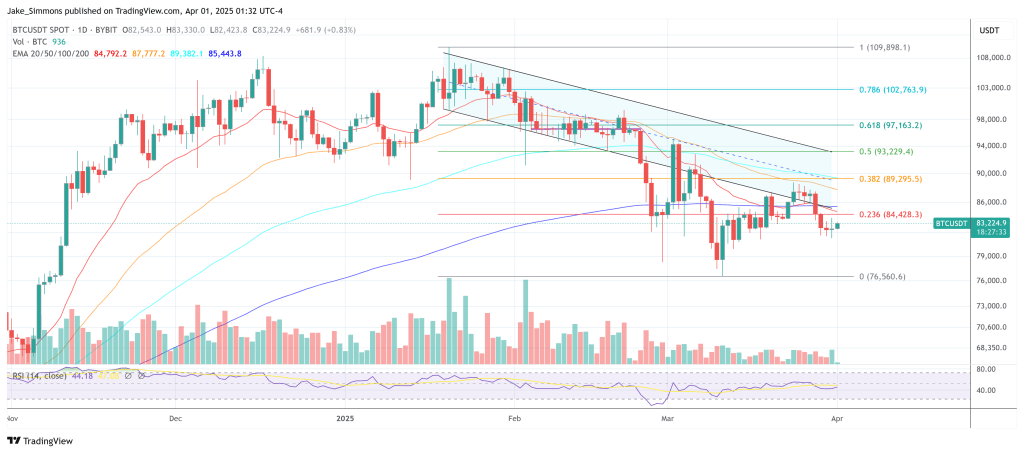

At press time, BTC traded at $83,224.